Trends in Large Language Models and Their Applications in Quantitative Investing

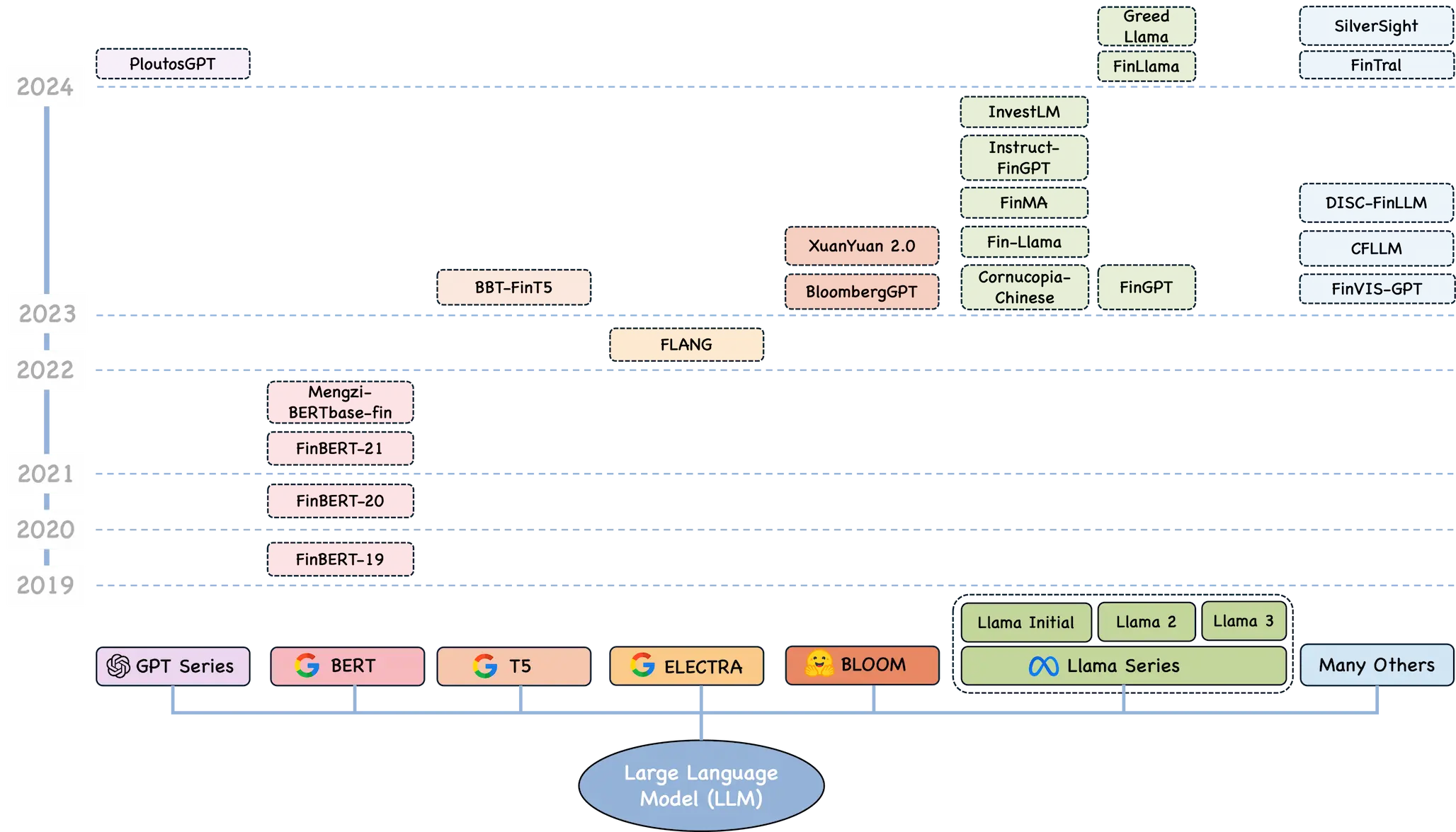

Large language models have become the hottest and fastest-moving frontier in computing since ChatGPT burst onto the scene at the end of 2022. LLMs have gradually shed the role of mere tools and become independent carriers of intelligence that can handle tasks on their own. In 2024, hundred-billion-parameter models such as Qwen2 and Llama3.1 were released one after another, and the performance of open-source models has moved steadily closer to that of closed-source systems. For quantitative researchers, a necessary question is how to combine LLM technology with financial applications to improve research and investment. This article first draws on Li Mu’s talk to discuss LLM trends and best practices, and then reviews specific application scenarios for LLMs in quantitative investing.