When things reach an impasse, change becomes possible; through change comes flow; through flow comes endurance.

The techniques of markets change without cease. High-frequency market making chases light at the microsecond scale; on-chain protocols build pools of liquidity with mathematics; spot-futures arbitrage searches across different time horizons for the pull of equilibrium. There are countless methods.

And yet the Great Way is simple, and all methods return to one origin. There is a path that does not cling to technique but wanders through principle, turning complexity back into simplicity: the practice of the “generalized liquidity provider” (LP). Those who follow it eventually see that market making and arbitrage are merely two sides of the same coin, each rooted in the other.

These notes are a record of that practice. What they seek is not a bag of tricks, but a way that runs through the whole system: a unified underlying framework for every form of liquidity provision. Only then can one build durable understanding in a market that never stands still, and ultimately move in harmony with it.

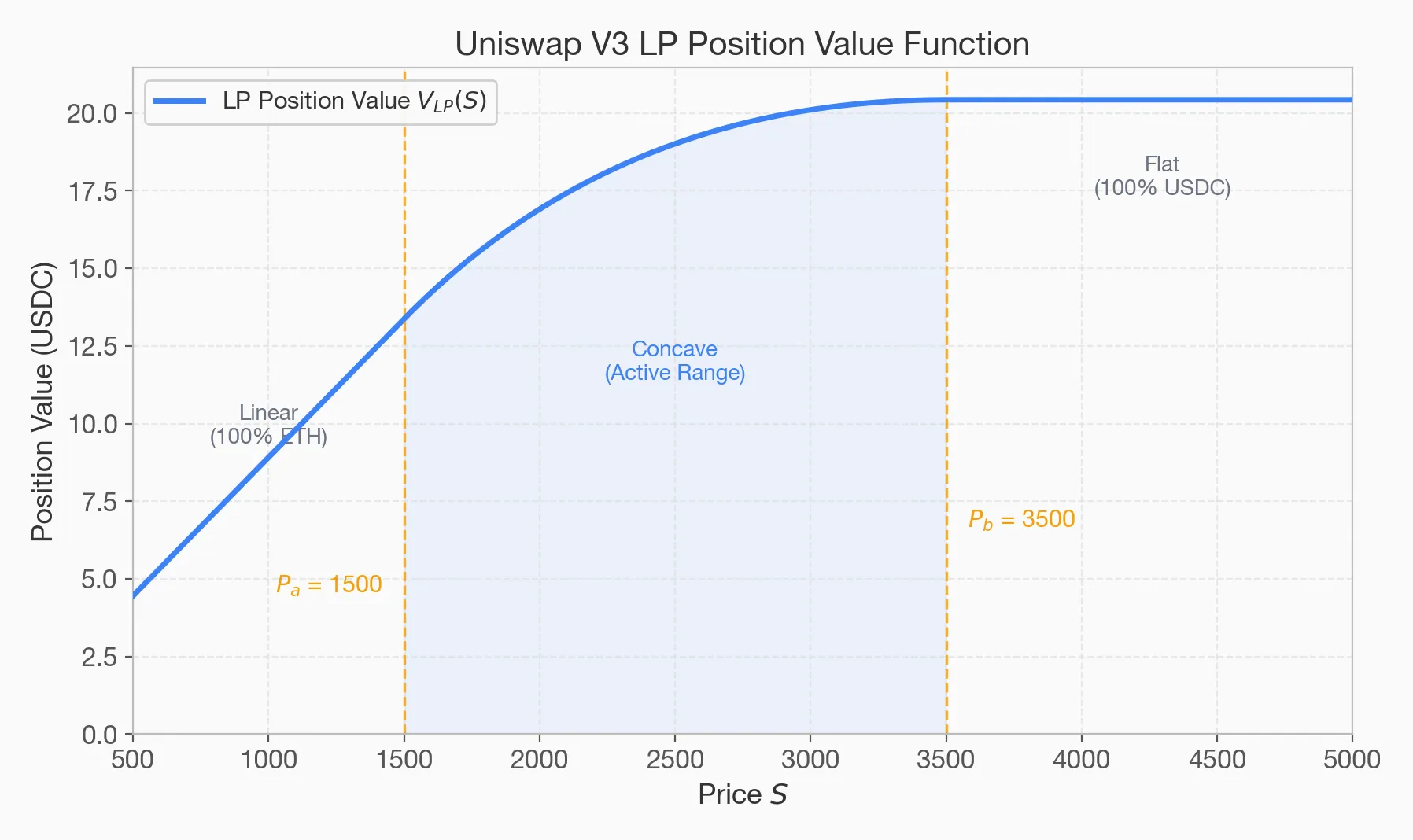

![[AMM Quant Deep Dive 01] Understanding the Economic Essence of AMMs: From Impermanent Loss (IL) to Loss-Versus-Rebalancing (LVR)](/./AMM1/cover.webp)