A Funding-Rate Arbitrage Strategy for Crypto Perpetual Futures

This strategy captures low-risk arbitrage opportunities in the cryptocurrency market through the funding-rate mechanism and staking yield.

Strategy Logic

Funding Rate

Mechanism

Exchanges establish a funding mechanism to ensure that perpetual-futures prices reflect changes in the underlying market. The mechanism causes long-position holders and short-position holders to exchange cash flows periodically so that the perpetual contract price converges toward the index price. When the funding rate is positive, long holders pay funding to short holders. When the funding rate is negative, short holders pay funding to long holders. Funding is settled once every eight hours.

For an inverse contract, the position value is

Position value = number of contracts × contract face value × contract multiplier / mark price

Example: a user holds a short position of 100 ETHUSD perpetual contracts. The current mark price is 4,000 USD, the contract face value is 10 USD, and the funding rate is 0.1%.

Position value = 100 × 10 × 1 / 4,000 = 0.25 ETH

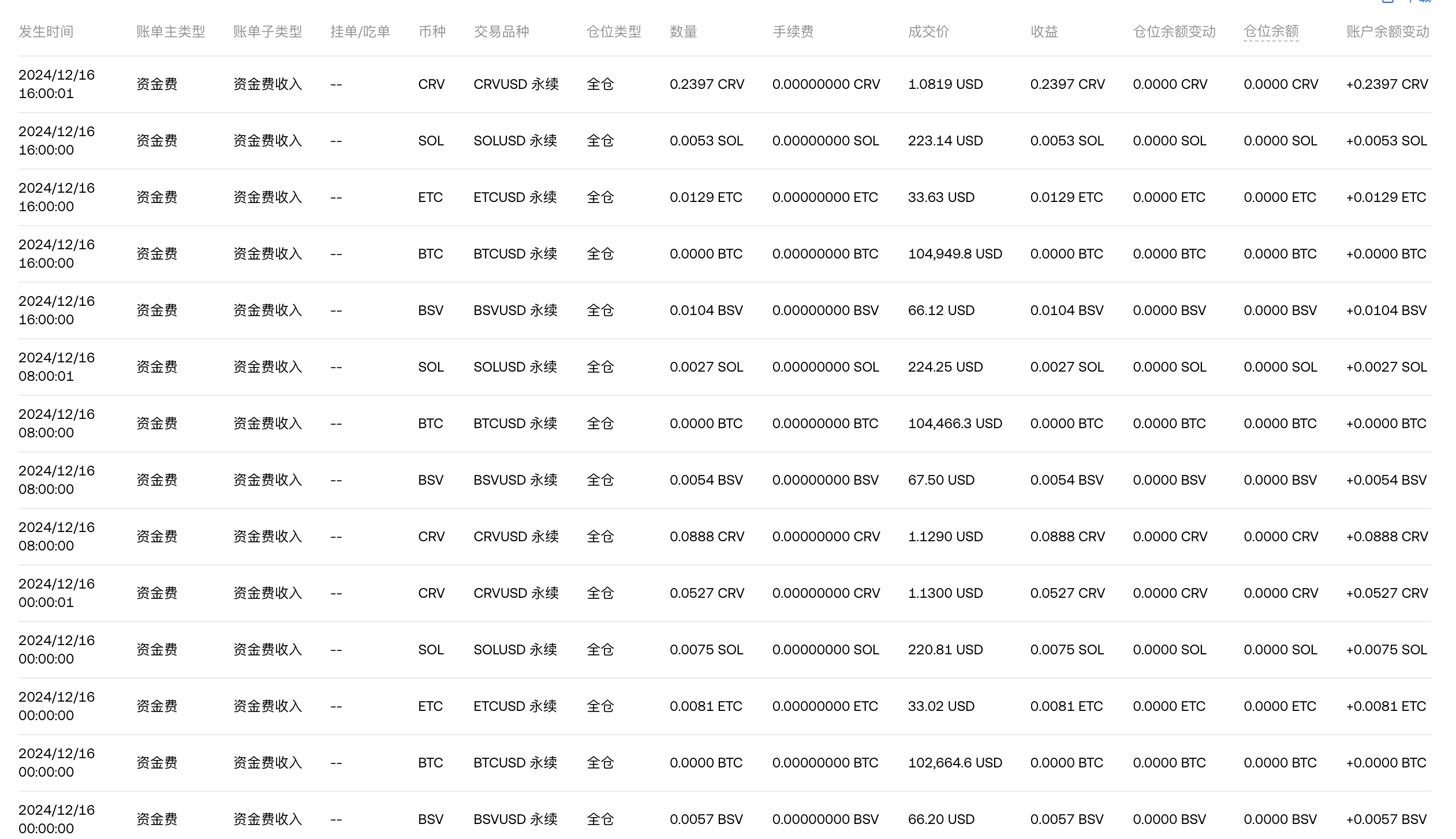

Funding payment = 0.25 × 0.1% = +0.00025 ETH

The funding payment is credited directly by the exchange to the user’s trading account.

Return Analysis

Funding rates are driven by the fixed interest component and market premium, and the combination of the two creates the possibility of positive long-run returns. Binance, for example, uses a fixed interest component and assumes that the interest earned on holding cash equivalents is higher than the interest earned on holding an equivalent amount of BTC. Binance’s contract interest is preset at 0.03% per day. Since funding is computed every eight hours, that means 0.01% per funding interval, which is about 11% annualized. Premium index (P) = [Max(0, impact bid - price index) - Max(0, price index - impact ask)] / price index

These two factors make cumulative funding payments usually positive:

- the base interest component is positive

- retail traders prefer to use leverage to go long in futures rather than go short. The first trade opened by most futures traders is a long position, because making money on the upside is more intuitive and rising prices leave unlimited room for imagination, while short-side gains are limited.

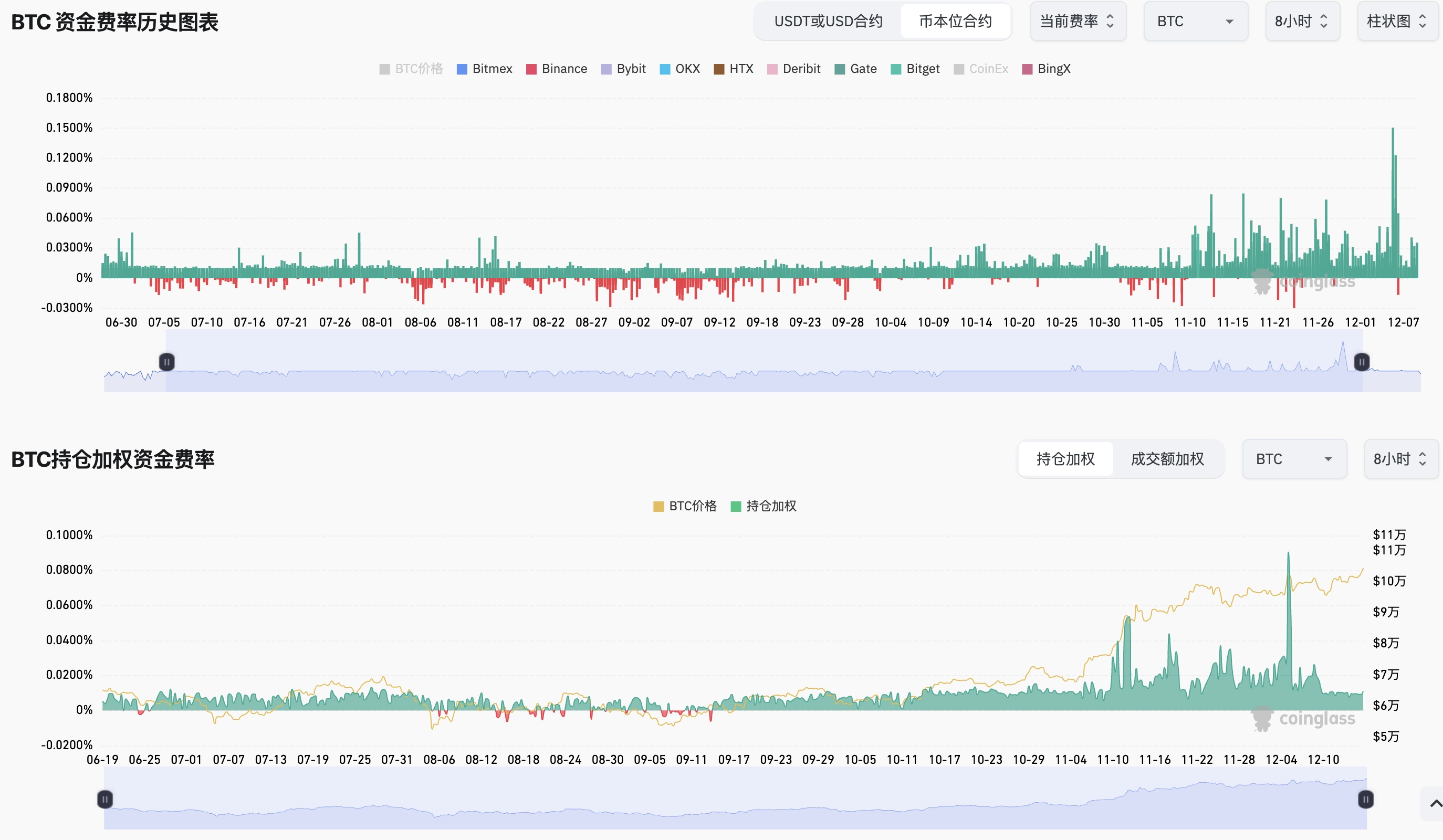

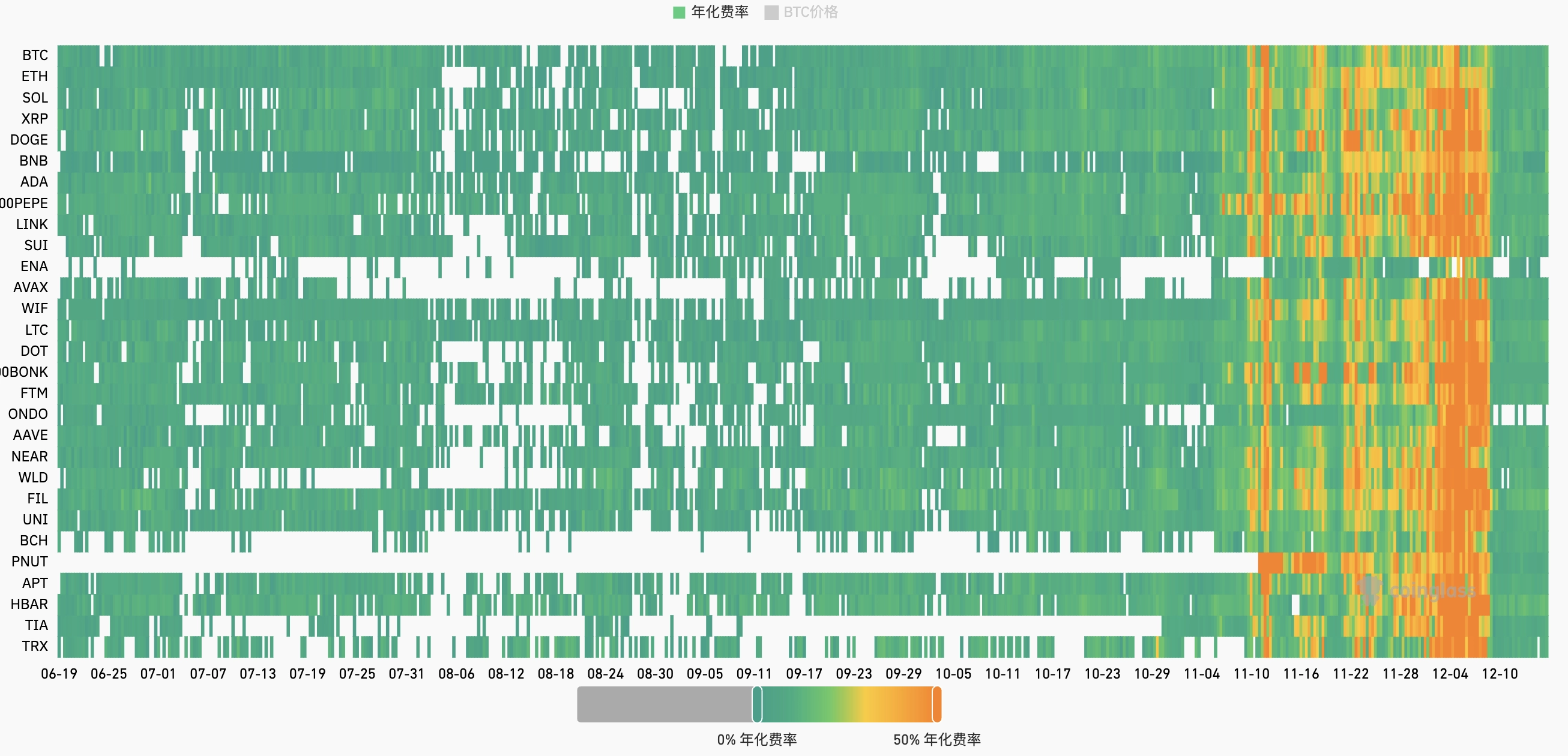

Historical data across major exchanges shows that for most coins, funding rates are positive most of the time and display strong persistence.

Inverse-Contract Arbitrage

The best way to harvest funding is to sell inverse perpetual contracts. Traditional arbitrage holds spot together with a USDT-margined perpetual for risk hedging, but that leaves two problems:

- low capital efficiency. For example, if 75% of the capital buys spot and 25% is used as futures margin at 3x leverage, the return rate is diluted.

- liquidation risk. Even at 1x leverage, liquidation can still occur.

Inverse contracts, also called coin-margined contracts, use the cryptocurrency itself as margin. After buying spot, the strategy uses the spot asset as margin to open a short position, which raises capital efficiency to 100%. At the same time, if the coin price rises, the margin value rises as well. Under the inverse-contract mechanism, a 1x short position has no liquidation risk.

The return of perpetual-futures arbitrage comes from funding and basis.

- funding rate As discussed above, the long-run annualized funding yield is around 15%, and in bull markets it can be 30% to 50%. During execution the strategy predicts and rotates into contracts with high short-term funding, with an expected annualized return above 20%.

- basis spread The spread also affects short-term returns. Because spot-futures arbitrageurs exist, the basis is usually within 0.1%.

- At entry, the basis is treated as part of trading cost.

- After entry, if the premium rises, the futures leg shows a floating loss, but the higher premium also raises the funding rate, penalizing longs and rewarding shorts, which is favorable for long holding periods.

- After entry, if the premium falls, profits can be realized from the spread, and the strategy can consider exiting and switching to another pair.

Staking Yield

For certain special tokens such as ETH and SOL, returns can be enhanced through on-chain staking without increasing leverage.

Staked tokens can earn additional yield, for example, a current annualized staking yield on SOL of more than 11%. The reason staking SOL produces return is tied to the Proof of Stake consensus mechanism of the blockchain network. When SOL is staked, the tokens are delegated to validator nodes, which use them to participate in network consensus, package blocks, and verify transactions. In return, the network gives validators block rewards and a share of transaction fees, mainly through inflation rewards and priority fees paid by traders who want faster execution. These rewards rise when network activity is heavy.

Staking the native token does not increase leverage and still carries no liquidation risk. The mechanism is that when assets are staked through an exchange, the platform issues a liquid staking token as proof of the staked position, such as OKSOL for staked SOL. OKSOL can be exchanged 1:1 for SOL, and their values remain nearly identical. That makes it possible to transfer OKSOL into the trading account as cross-asset margin and use it in place of spot SOL.

Quantitative Implementation

Low-risk arbitrage can often be executed manually, but automation enables smarter rotation across instruments and more refined trade execution.

A Supervised-Learning Framework for Instrument Rotation

Assume the following:

- The trading cost \(c_i\) is fixed and is paid only once at entry, independent of holding period.

- Borrowing the idea of a reinforcement-learning reward, the target for each coin is the weighted sum of future funding rates, that is, the discounted cumulative funding return.

For coin \(i\), define the weighted sum of future funding rates as

$$ G_i = \sum_{k=1}^T \gamma^{k-1} \hat{r}_i^{t+k} - c_i $$

where:

- \(\hat{r}_i^{t+k}\) is the funding rate in future period \(k\)

- \(\gamma \in (0, 1]\) is the discount factor that controls the weight on future returns

- \(c_i\) is the entry cost, including fees, price impact, and basis spread

The core of the strategy is to predict \(G_i\) for each coin. That can be done directly with machine learning or time-series modeling:

Each coin’s dataset includes its historical funding-rate sequence \([r_i^{t-k}, \dots, r_i^t]\) and the target value \(\hat{r}_i^{t+k}\).

Feature design:

- historical funding rates \([r_i^{t-k}, \dots, r_i^t]\)

- market features such as price volatility and trading volume

- technical indicators such as moving averages and volatility

Use a machine-learning model such as an LSTM, Transformer, or classical regression model to predict the weighted sum of funding rates:

$$ \hat{G}_i = f_\theta(s_i) $$

where:

- \(s_i = {r_i^{t-k}, \dots, r_i^t, \text{other features}}\) is the input feature set

- \(f_\theta\) is the prediction model and outputs the estimated cumulative return for coin \(i\)

The target is to minimize prediction error:

$$ \mathcal{L} = \frac{1}{N} \sum_{i=1}^N \left( \hat{G}_i - G_i \right)^2 $$

At each time step \(t\), the strategy opens a short in the coin with the highest predicted \(\hat{G}_i\):

$$ i^* = \arg\max_i \hat{G}_i $$

This method is efficient, intuitive, and easy to implement while keeping the core objective of return maximization intact.

Trade Execution

The arbitrage logic above requires trades in both spot and futures markets, and manual execution can easily introduce delay and temporary risk exposure. To reduce trading fees, the better approach is to place the order in futures first and, once it fills, immediately sell the spot leg at market so that market exposure stays neutral. During rotation, the strategy can search for the optimal execution path in the graph formed by trading pairs, for example BTC->ETH->SOL or BTC->USDT->SOL.

A Funding-Rate Arbitrage Strategy for Crypto Perpetual Futures