Behavioral Finance in Factor Investing: From Positional Warfare to Psychological Warfare

Traditional finance assumes that market participants are perfectly rational, which is obviously at odds with reality, so it cannot explain the many forms of mispricing that appear in practice. Behavioral finance treats investors as boundedly rational and combines traditional financial theory with psychology to study which irrational behaviors create mispricing and how those biases connect to asset returns. Factor investing treats human behavioral bias as a source of excess return, so it is worth reviewing the main results of behavioral finance as a whole and linking them to the anomalies seen in markets.

Mispricing and Arbitrage

Humanity has built modern financial markets, but our genes are still not very different from those of our ancestors. People generally possess physiological and psychological traits selected for survival and reproduction. Under deep-seated cognitive bias, they make large numbers of irrational decisions that lead assets to become overvalued or undervalued. Rational investors, including factor investors, can arbitrage such mispricing by buying undervalued assets and shorting overvalued ones, continuously earning excess returns from irrational investors. On the macro level this is rationality punishing irrationality; on the micro level the presence of arbitrageurs prevents prices from drifting even farther away from intrinsic value and keeps the trading terms faced by noise traders from worsening further.

Yet even though arbitrageurs exist, mispricing does not disappear in an absolute sense because limits to arbitrage remain. In some cases it can persist for quite a long time. Discovering and executing arbitrage opportunities both require extra cost, and while holding a position the investor must still bear the risk of sudden deterioration in fundamentals and short-term price volatility.

Irrational Expectations

Heuristics The brain often uses shortcuts to reduce the complexity of information processing. In psychology this is called heuristic simplification. Shortcuts such as representativeness and familiarity make investors analyze new information incorrectly and arrive at wrong conclusions. In financial markets, investors often confuse a good company with a good investment and love growth stocks whose earnings keep rising. Investors also tend to extrapolate past stock returns mechanically into the future, which ultimately leads to buying high and selling low; the short-term reversal effect is especially notable in A-shares. In addition, investors prefer markets and companies they are familiar with, and even a company name that simply sounds pleasant can raise trading volume.

Anchoring Anchoring means relying too heavily on the initial information provided when making a decision, even when that information has nothing to do with the decision itself. A classic finance example is George and Hwang (2004), which argues that the 52-week high is an important anchor. The closer a stock is to that high, the less aggressively investors react, causing underreaction. As a result, the momentum effect is stronger among stocks trading near their 52-week highs.

Overconfidence Overconfidence is a deeply rooted bias that appears mainly in two forms:

- people are more confident in their judgments than those judgments are accurate

- people think they are better than others, or that their judgments are more accurate than other people’s

When people are given room to act, they become more confident and feel they control the situation completely, even when they do not. For example, trading volume jumped after the spread of electronic trading. Overconfident investors often trade more, but high turnover is usually associated with lower expected returns and higher friction costs.

Optimism and conservatism Optimism is an inborn instinct. People tend to feel that outcomes are controllable and can unfold as expected, and a few lucky results reinforce that illusion. At the same time, when change is required, people wrongly take sunk costs into account and lean toward conservatism. Under this bias, investment managers often refuse to overturn earlier decisions even when the market has already shown that the original plan was wrong.

Confirmation bias Also called confirmatory bias, this means that people selectively recall and collect favorable details while ignoring unfavorable or contradictory information, all to support an existing view. Investors tend to gather confirming evidence instead of evaluating all available information. Similarly, when trapped in a losing trade, traders may refuse to accept reality and instead search desperately for every possible piece of evidence that supports their position, losing themselves in the process.

Limited attention Traditional finance argues that people should use all available information when making decisions. In reality, the brain has limited information-processing capacity. At any given moment it cannot handle all information in time and instead prefers to respond to the most salient and important inputs. This cognitive constraint is known as limited attention.

Biases in Risk Preference

Finance is full of uncertainty, and people also show bias in their attitude toward risk and in how they make decisions under uncertainty.

Risk exposure In investing, people’s risk preferences are not fixed in advance and then matched to a portfolio. They change dynamically. After making money, people become willing to bear more risk because they feel they are gambling with “house money.” After taking losses, they often become less willing to take risk. That said, some losing gamblers also increase their risk exposure and take larger bets in the hope of winning back principal. In either direction, letting prior gains or losses change one’s risk exposure is irrational behavior.

Ambiguity aversion In risk decisions, if the distribution of outcomes is known, the uncertainty of the decision is itself known and can be quantified precisely from that distribution. If the distribution is unknown, then the uncertainty is also unknown and cannot be measured accurately. Because of ambiguity aversion, people tend to choose against ambiguity and prefer what they know. In investing, that means people select targets that fit their own experience, knowledge, and ability.

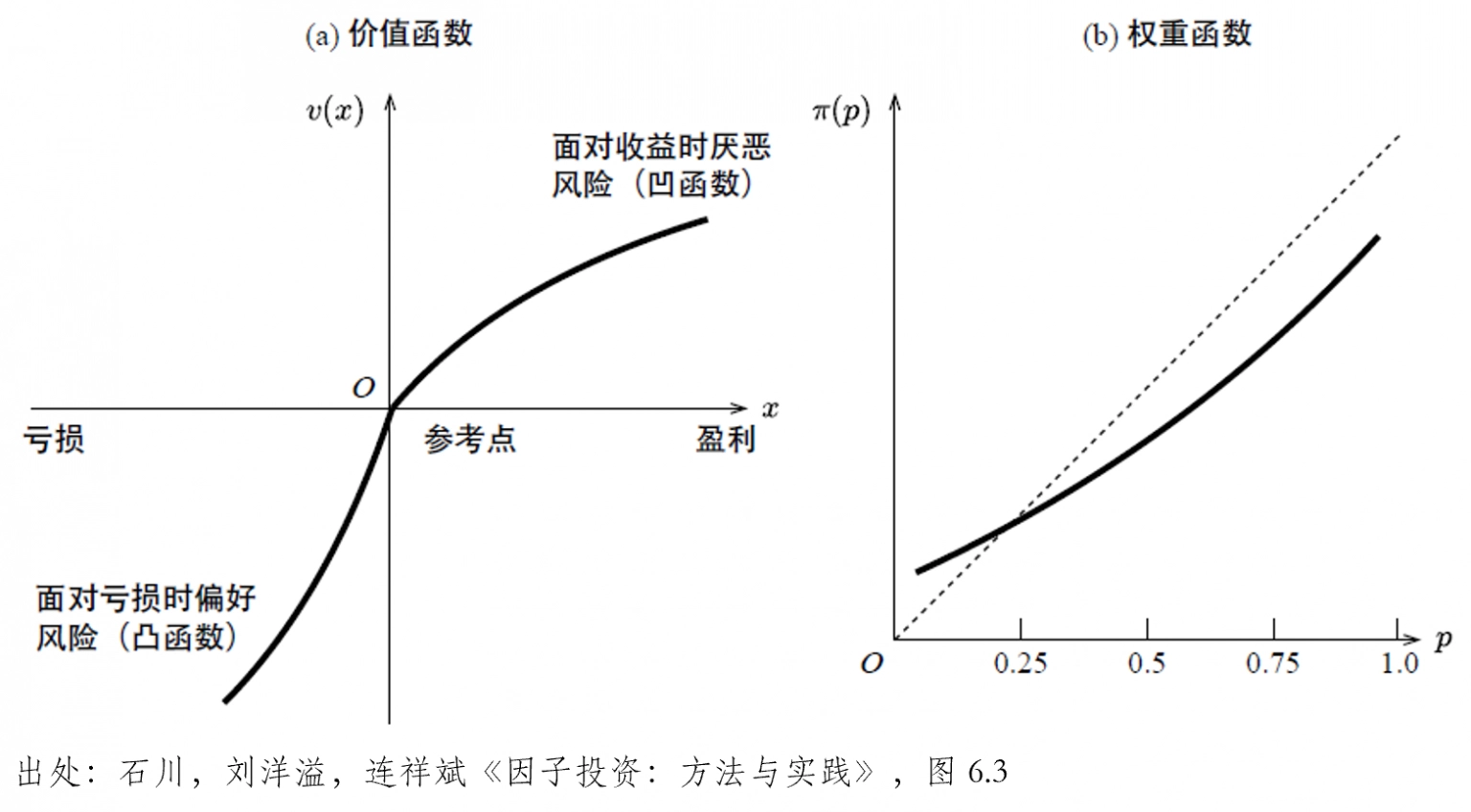

Prospect theory Proposed by psychologists Daniel Kahneman and Amos Tversky (Kahneman and Tversky 1979, Tversky and Kahneman 1992), prospect theory is an analytical framework for how people make decisions under uncertainty. At its core are the value function \(v(\cdot)\) and the weighting function \(\pi(\cdot)\) assigned to possible outcomes.

The shape of the value function shows that attitudes toward gains are not linear. First, people judge outcomes relative to a reference point and are more averse to losses. Second, sensitivity diminishes for both gains and losses. This shape explains the urge to lock in gains and the tendency to hold on to losers, which is the disposition effect. On the weighting-function side, compared with the true probability \(p\), people overweight small-probability events. That helps explain why so many people buy lottery tickets with negative expected value.

Salience theory Salience theory argues that in cross-sectional comparisons of assets, investor attention is drawn to the payoffs that are most salient on average, while less salient payoffs are often ignored. Investors therefore attach different psychological weights to different payoff magnitudes. Expressing this bias quantitatively helps describe more precisely how far prices deviate from true value. Comparing prospect theory with salience theory shows the difference clearly: in prospect theory the weighting bias comes from giving higher weight to small-probability tail events, while in salience theory extreme payoffs are weighted not because they are unlikely, but because they stand out relative to the market average in the cross section. The salience-theory model says asset premia are driven not by investor preference itself but by how much an asset’s payoff stands out from the market average, which incorporates both time-series and cross-sectional information.

Mental accounting In theory, one hundred yuan always equals one hundred yuan, but people mentally divide assets into different buckets and fail to make globally optimal decisions. For example, someone may save money for a trip while taking out a car loan at the same time, which obviously adds extra cost. Likewise, the common advice to put part of one’s money into low-risk assets and part into high-risk assets ignores covariance and therefore does not satisfy modern portfolio theory.

Behavioral Finance and Market Anomalies

Post-Earnings-Announcement Drift PEAD refers to continued price drift after an earnings release because limited attention causes investors to underreact to new fundamental information. From the perspective of investor sentiment, when earnings news beats expectations, investors may cling to prior beliefs out of conservatism and underreact to the surprise. They treat the good news skeptically and are reluctant to update their understanding of the firm’s fundamentals, so the information is not immediately reflected in the stock price.

Prospect theory The weighting function in prospect theory can explain the famous skewness anomaly, namely that right-skewed “lottery-like” stocks have lower expected returns. The value function can explain the disposition effect: investors often fail to hold winners and prefer to sell after profits, yet hesitate to sell losers. In the literature, unrealized gains are usually measured with capital gain overhang, or CGO.

$$ RP_t=\frac{1}{k} \sum_{n=1}^{100}\left({~V}_{t-n} \prod_{s=1}^{n-1} \left( 1-V_{t-n+s}\right) \right) {P}_{t-n} $$

$$ CGO = \frac{P_t}{RP}_t-1 $$

Salience theory Based on salience theory, Cosemans et al. (2021) construct the ST indicator to recover the psychology behind investor decisions. When ST is positive, the stock’s highest payoff stands out more strongly, causing investors to overfocus on upside potential and behave like risk seekers. When investors focus excessively on negative payoffs and emphasize downside risk, ST becomes negative, and the related stocks tend to be overly undervalued.

In this framework, stock-level salience depends on both stock returns and benchmark returns. A later report by GF Securities linked stock salience to turnover and also found good empirical results.

$$ \sigma\left(r_{i, s}, \bar{r}_{s}\right)=\frac{\left|r_{i, s}-\bar{r}_{s}\right|}{\left|r_{i, s}\right|+\left|\bar{r}_{s}\right|+\theta} $$

Regret aversion Under regret aversion, people make decisions in ways that reinforce self-approval and avoid feelings of regret. In markets this can show up as continuing to hold after buying into a loss and refusing to buy back after selling a rising stock. Using the closing price as a psychological anchor, Guojin Securities built regret-aversion factors to measure this mentality: the share of buy volume executed above the close, the share of sell volume executed below the close, the average purchase price of underwater positions, and the average sale price on rising days. The basic logic is that the higher the fraction of buy volume executed above the close, the stronger the day’s buying sentiment and the larger the unrealized-loss share, which means lower future selling pressure and higher expected returns. Similarly, the farther the purchase price above the close, the more severe the unrealized loss and the lower the future selling pressure, again implying higher expected returns. By contrast, stocks with a higher share of sell volume executed below the close, or a larger downward deviation from the close in those sales, leave investors less willing to buy back because of the psychological effect of having sold. Such stocks then have weaker future buying support and lower expected returns. Splitting the data further by order size and trading session improves the factor performance.

Behavioral Finance in Factor Investing: From Positional Warfare to Psychological Warfare