Volume Factors: Turnover and Illiquidity

Trading volume is an indispensable part of the volume price factor, but in most cases it appears as a supporting role in the coordination of volume and price, as discussed in Volume Price Relationship Factor and Momentum Reversal Factor. This article focuses on the trading volume itself and discusses two important stock selection factors: turnover factor and illiquidity premium. The trading volume factor has significant predictive effect on stock cross-sectional returns in global markets, especially in immature markets such as A-shares.

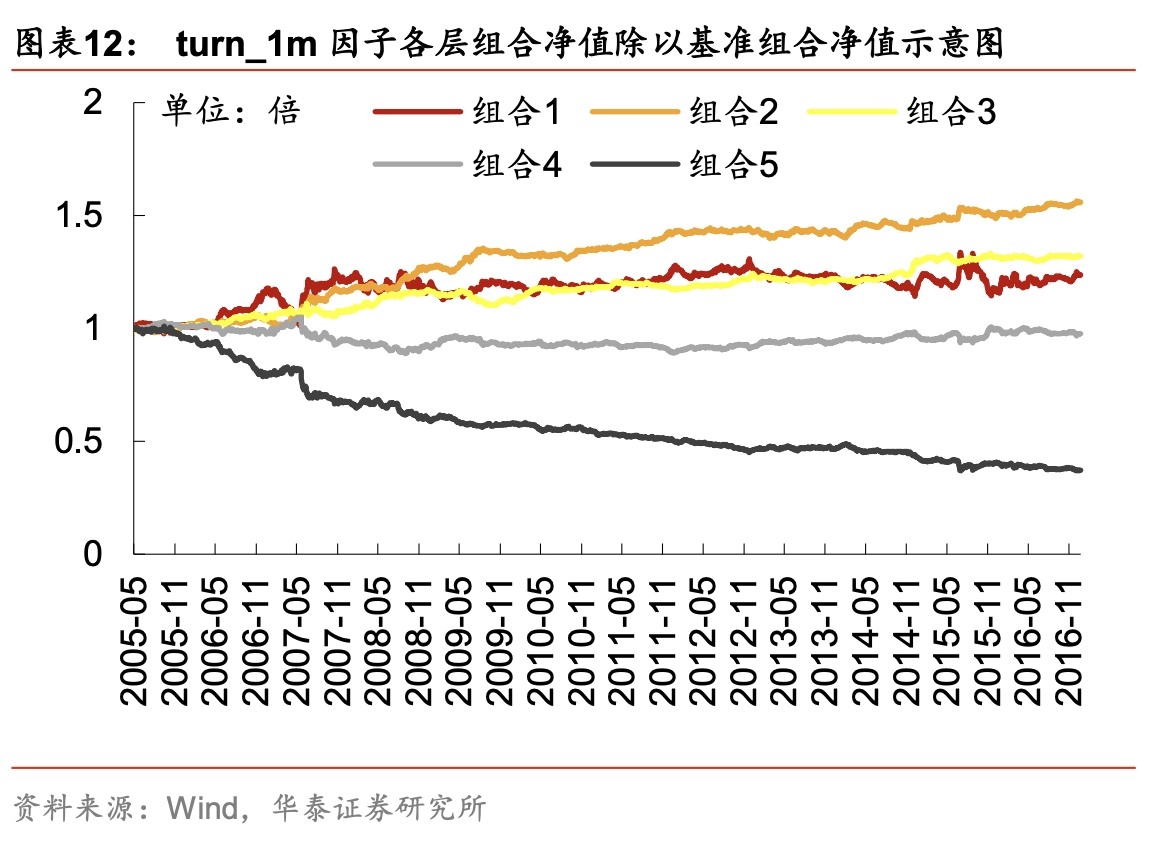

Daily turnover rate

Both theory and empirical evidence show that turnover rate is negatively correlated with expected returns, and to a certain extent, it can explain each other with low volatility and short-term reversal anomalies. From the perspective of behavioral finance, high turnover rates reflect investors’ irrational emotions, such as overconfidence and blind optimism, and other expected deviations, and therefore can be regarded as an emotional indicator. At the same time, high trading volume means there are stronger differences among investors and greater uncertainty about future trends. Investors have limited attention and can only process limited information within a period of time. Therefore, stocks with a high turnover rate have higher visibility. As star stocks, they attract more potential buyers and may obtain higher short-term returns, but their long-term performance is poor.

In the practice of A-shares, the following turnover factors are commonly used: average turnover rate, volatility of turnover rate, abnormal turnover rate (the ratio of short-term turnover rate to long-term turnover rate), and abnormal turnover rate. There are significant differences in turnover factors among different industries and market capitalization stocks. Therefore, direct cross-industry comparisons of listed companies are of little significance. Neutralization of market capitalization industries will achieve better results. The long-term performance of the turnover rate factor is very stable. Unfortunately, the factor IC is mainly contributed by short sellers and the long sellers perform poorly. In practice, turnover rate may be used as a reliable short-short elimination indicator, but it alone cannot contribute stable alpha returns.

High frequency transaction distribution

The data used in the turnover rate factor is relatively simple, so China Merchants Securities proposed to use intraday high-frequency data to examine the persistence of abnormal trading volume within the day, and proposed the PATV factor of continuous abnormal trading volume. PATV has better monotonicity and more significant long returns. PATV first measures the relative level of a stock’s abnormal trading volume in a certain minute in the entire market by calculating the percentile rank_ATV of each stock’s intraday abnormal trading volume ATV in the entire market. Each day, the mean value of rank_ATV is divided by the standard deviation, plus its kurtosis, as the PATV indicator for that day, and the final factor is obtained after the moving average.

PATV is the continuation of the daily frequency turnover rate factor idea in high-frequency data. At the same time, there are also some statistical indicators for high-frequency trading volume. Similar to the [Intraday High Frequency Volatility Decomposition] (https://heth.ink/HighFreqVol/) measure of intraday high frequency return distribution, we can first calculate indicators such as the central moment of high frequency trading volume distribution, such as standard deviation, deviation, kurtosis, and information entropy. At the same time, as mentioned in idiosyncratic volatility factor, by decomposing the trading volume into a common part and an idiosyncratic part, indicators such as idiosyncratic skewness and idiosyncratic kurtosis can be calculated. The improvement is not as great as the idiosyncratic rate of return, but the original framework can be reused, which is worse than nothing after all.

The distribution of trading volume in different time periods also has different properties. For example, if the trading volume in the early and late trading is too large, it is associated with negative expected returns; the intraday trading volume is a positive stock selection factor.

Illiquidity Premium

If some stocks are less liquid and investors have to pay larger transaction costs for transactions, then a liquidity premium is theoretically required. Amihud2002 defines the illiquidity proxy variable as the average return change corresponding to unit transaction volume. Overnight price movements are typically driven by the arrival of information, and the price changes caused by the arrival of these information are independent of the daily trading volume used in the denominator of the ILLIQ indicator. Compared with the illiquidity factor constructed using intraday absolute returns as the numerator, the IC mean and t-statistics of the illiquidity factor constructed using intraday absolute returns as the numerator are improved.

$$ ILLIQ=\frac{|r|}{vol} $$

We can improve the ILLIQ factor from the Taylor expansion perspective

$$ ILLIQ2=E\left(\left|r_{i, d}\right| / {vol}_{i, d}\right)=E\left(\left|r_{i, d}\right|\right) \cdot E\left(1 / {vol}_{i, d}\right)+\operatorname{cov}\left(\left|r_{i, d}\right|, 1 / {vol}_{i, d}\right) $$

Among them

$$ \operatorname{cov}\left(\left|r_{i, d}\right|, 1 / \operatorname{vol}_{i, d}\right) \approx-\frac{\operatorname{cov}\left(\left|r_{i, d}\right|, \operatorname{vol}_{i, d}\right)}{\left(E\left[\operatorname{vol}_{i, d}\right]\right)^{2}} $$

Similar to SemiBeta, illiquidity also has different properties when the stock price rises/falls. Logically speaking, illiquidity is more fatal to investors when the stock price falls and requires a higher risk premium.

$$ SemiILLIQ=\frac{|min\{r, 0\}|}{vol} $$

Essentially, the illiquidity factor measures how price changes with volume. Lamda factor, also known as price shock elasticity, is defined as the regression coefficient of return on signed trading volume. All the above non-current factors can also be rewritten as high-frequency implementation, and the effect is similar.

Volume Factors: Turnover and Illiquidity